Introduction

Download the complete PDF documentation here.

Markowitz portfolio theory is used in investment management

as a tool for diversifying away risk through portfolio balancing.

Given a set of investment assets, it finds the most efficient

allocation (portfolio weights). Here, efficiency is defined

as minimizing the expected variance. Markowitz portfolios

may be subject to specified constraints, such as a specific

return on investment (expected price), non-negativity

constraints (restricting short selling), and may include

risk-free assets or market indices [1].

This example will select a minimum variance portfolio,

constrained to a specified expected rate of return.

All results will be annualized as commonly reported to

investors.

Implementation

This optmization problem may be expressed as minimizing the portfolio variance,

subject to the constraint that the individual allocation weights of the stocks add to unity,

and the expected return is equal to the specified target.

$$

\begin{equation*}

\begin{aligned}

& \underset{w}{\text{minimize}}

& & \mathbf{\sigma}_{p,w}^2 = \mathbf{w}^T \mathbf{\Sigma} \mathbf{w} \\

& \text{subject to}

& & \mu_{opt} = \mathbf{w}^T \mathbf{\mu} \\

&

& & \mathbf{w}^T \mathbf{\underline{1}} = 1

\end{aligned}

\label{eq:optimization_problem}

\end{equation*}

$$

Where

$$

\begin{align}

\begin{array}{cl}

\mathbf{\sigma}_{p,w}^2 & \mbox{portfolio variance of weighted assets} \\

\mathbf{w} & \mbox{individual asset weights} \\

\mathbf{\Sigma} & \mbox{covariance matrix} \\

\mathbf{\mu} & \mbox{individual asset returns} \\

\mathbf{\mu}_{opt} & \mbox{target portfolio return} \\

\end{array}

\end{align}

$$

Forming the Lagrangian function for the constrained minimization, we have

$$

\begin{equation}

L(w,\lambda_1,\lambda_2) = \mathbf{w}^T \mathbf{\Sigma} \mathbf{w} + \lambda_1 (\mathbf{w}^T \mathbf{\mu} - \mu_{opt})

\label{eq:lagrangian}

\end{equation}

$$

So the first order conditions are

$$

\begin{equation}

2 \partial L(w,\lambda_1,\lambda_2) = 2 \mathbf{\Sigma} \mathbf{w} + \lambda_1 \mathbf{\mu} + \lambda_2 \mathbf{\underline{1}} = \mathbf{\underline{0}}

\label{eq:foc1}

\end{equation}

$$

$$

\begin{equation}

\frac{2 \partial L(w,\lambda_1,\lambda_2)}{\partial \lambda_1} = \mathbf{w}^T \mathbf{\mu} - \mu_{opt} = 0

\label{eq:foc2}

\end{equation}

$$

$$

\begin{equation}

\frac{2 \partial L(w,\lambda_1,\lambda_2)}{\partial \lambda_2} = \mathbf{w}^T \mathbf{\underline{1}} - 1 = 0

\label{eq:foc3}

\end{equation}

$$

Expressed in matrix form

$$

\begin{equation}

\mathbf{A}\mathbf{x} =

\left[ \begin{array}{ccc}

2 \mathbf{\Sigma} & \mathbf{\mu} & \mathbf{\underline{1}} \\

\mathbf{\mu}^T & 0 & 0 \\

\mathbf{\underline{1}}^T & 0 & 0 \\

\end{array} \right]

=

\left[ \begin{array}{c}

\mathbf{w} \\

\lambda_1 \\

\lambda_2 \\

\end{array} \right]

\left[ \begin{array}{c}

\mathbf{\underline{0}}^T \\

\mu_{opt} \\

1 \\

\end{array} \right]

= \mathbf{b}

\label{eq:lineq_expand}

\end{equation}

$$

This may be solved for $\mathbf{b}$, where the first $n-2$ elements of $\mathbf{b}$ are the portfolio weights ($\mathbf{w}_{n} = \mathbf{b}_{n}$).

$$

\begin{equation}

\mathbf{b} = \mathbf{A}^{-1} \mathbf{x}

\label{eq:lineq_mat}

\end{equation}

$$

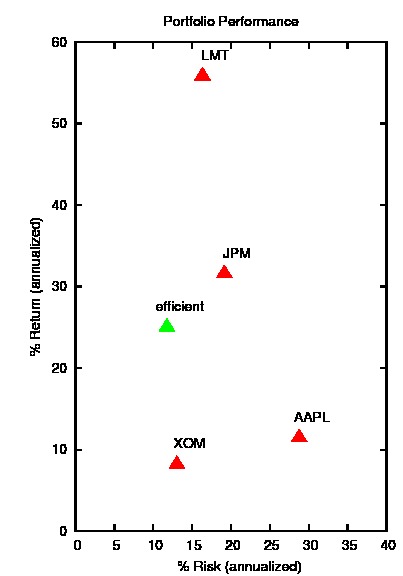

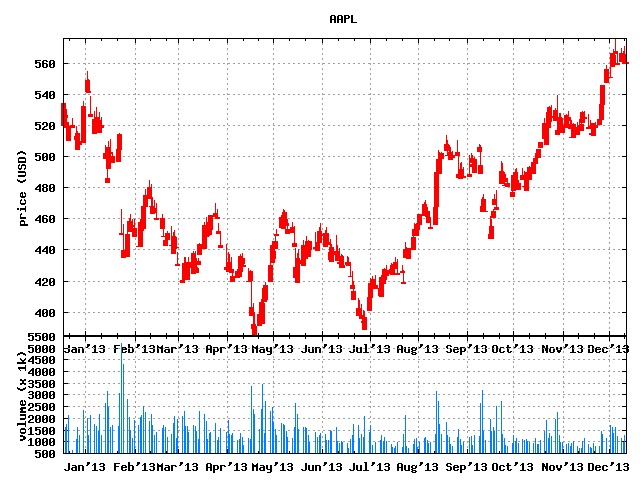

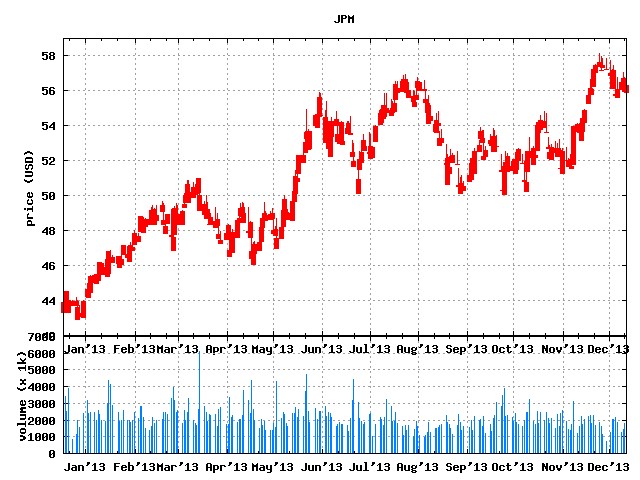

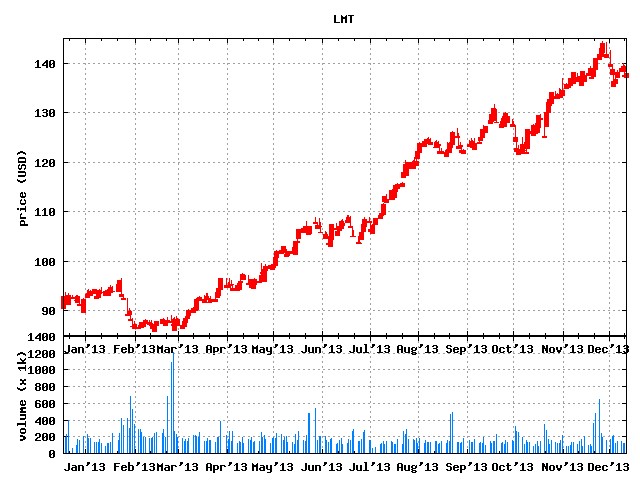

Example Portfolio #1: AAPL, JPM, LMT, XOM

$$

\begin{array}{ l l l l }

\textbf{Portfolio #1 (AAPL, JPM, LMT, XOM)} \\

\hline

\textbf{Symbol} & \textbf{Weight} & \textbf{ROI} & \textbf{Volatilty} \\ \hline

AAPL & 0.08 & 11.4\% & 28.8\% \\

JPM & 0.12 & 31.6\% & 19.1\% \\

LMT & 0.39 & 55.8\% & 16.3\% \\

XOM & 0.40 & 08.2\% & 13.0\% \\

\hline

portfolio & & 25.0\% & 11.76\% \\

\hline

\end{array}

$$

Historical Data

References

[1] Wikipedia. (2011, Aug.). Modern Portfolio Theory. [Online]. Available: http://en.wikipedia.org/wiki/Modern_portfolio_theory.